Financialization and Acceleration of India’s Wealth

Financialization and Acceleration of India’s Wealth

The other end of India’s increasing per-capita income

Hi,

Now we all have heard about how this is India’s decade, with good GDP growth and rapid expansion of per-capita income.

Now if India is set to see a rise in the income of its population, I was curious, what would that mean for the average wealth a person holds in the country?

The reason for the curioisity? I work for an industry that manages people’s money, and quite frankly, this is just validation for career choices.

So let’s dig in

Setting the Context - The growth in India’s per capita income

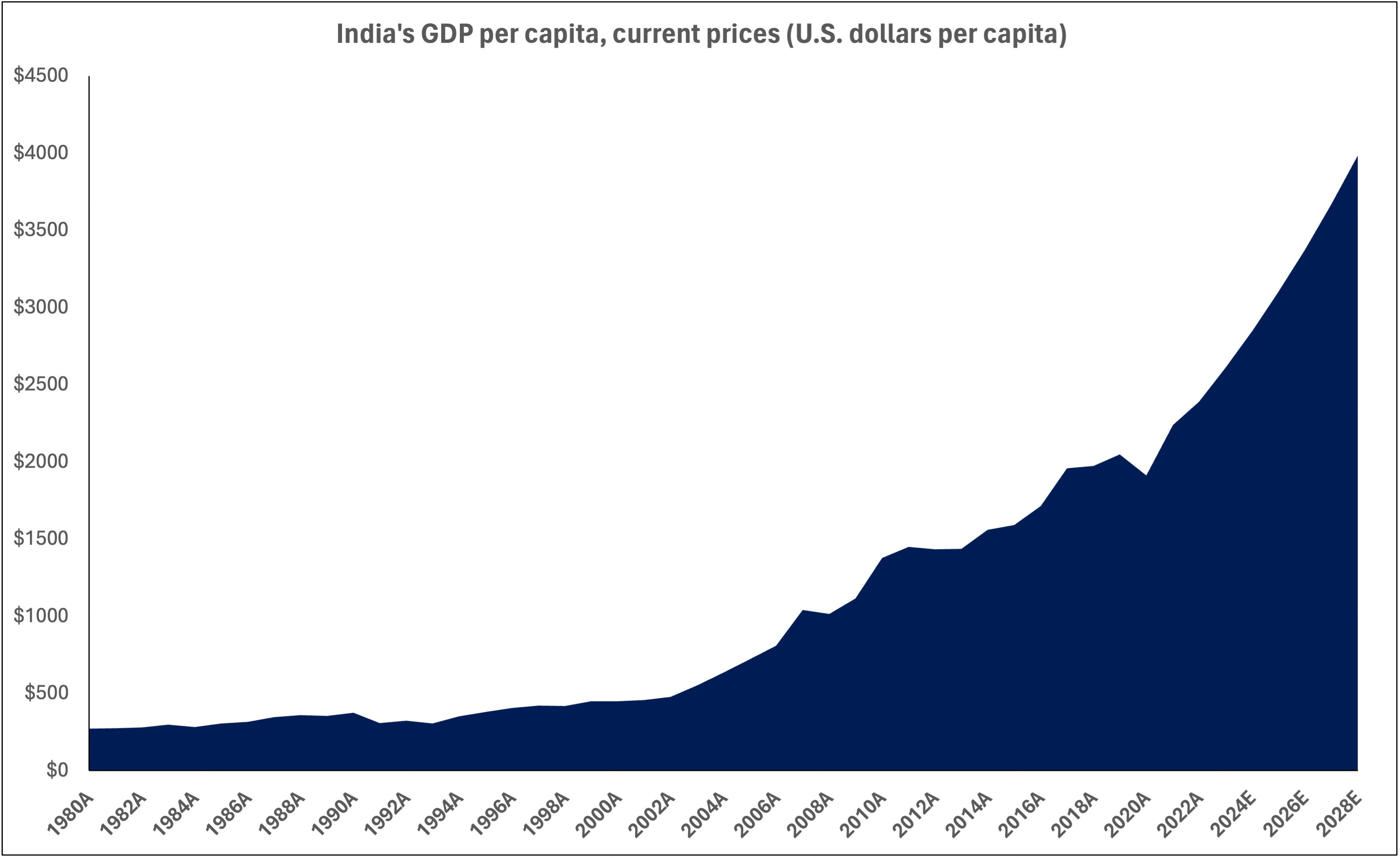

Now it’s a commonly made assumption that India’s GDP and the per-capita income both are set to rise exponentially, one of the reasons why this is a big talking point as well is that back in 2021, India crossed the $2,000 inflection point where the income is finally high enough for sustenance, and can be used for spending and investments.

Back in 1980s it was around the ~$350 mark, where as today it stands closer to ~$2,500 mark in 2023 and is all set to grow to $4,000 by 2028 - that’s ~60% jump expected in ~5 years.

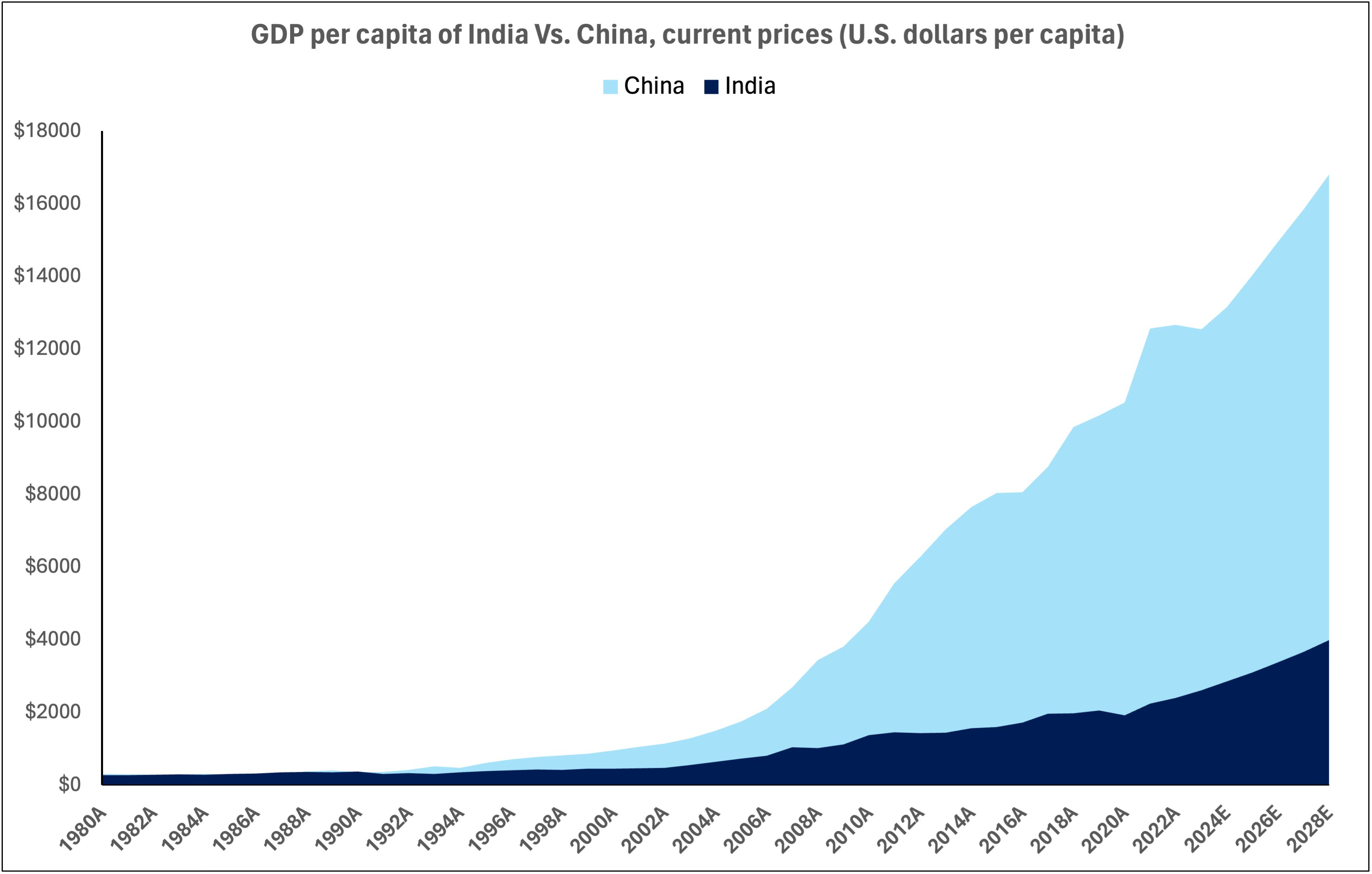

Now if that seems a tad bit unrealistic or seems like a large target; here’s India’s per capita income vs. China

Yup back in 1980, we started roughly at the same starting line but China ofcourse has gone all ballistic and is now sitting at a per-capita income of around ~$12,500 - so not so far fetched.

Now what allowed China to leap frog and drive it’s per-capita income to rise so fast? Public investment in Manufacturing - (I know, nothing new)

But there’s something more here, in recent years, household consumption has become a stronger contributor to their growth, infact the services sector also now accounts for more than half of their annual GDP and close to half of aggregate employment.

So fair to say; it was govt. investment into manufacturing > people found employment > country made money making and exporting goods to the world > money made was money spent back into economy > more money made

Now where India lacks is manufacturing; which seemingly is now becoming more in focus, with alot more countries talking about China +1

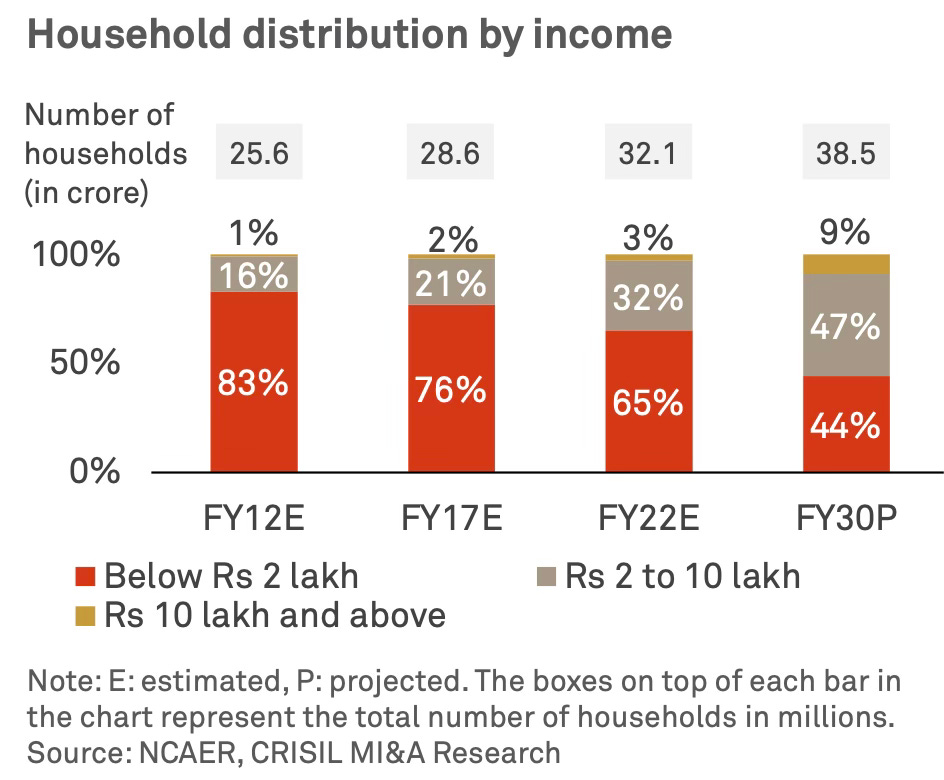

Given all that, the middle class is all set to expand as a % of households, leading to more people coming into the fray of discretionary expenditure and of investing in assets.

Now with that context sorted, let’s move on to main point here, Wealth!

How would the increased income reflect in wealth?

Now there are two aspects of this broad question

The quantum - how much can it become and how would it look it for everyone?

Where would it be invested

Let’s answer 1) first

The Quantum of Wealth Growth

In India, wealth per adult is at $16,500 in 2022, while the global average is at ~$85,000;

In terms of growth, the wealth per adult in India had a CAGR of ~7.5% between 2000-22; For context though, the wealth per adult of China has been growing at a much faster pace of ~12% in the same period, the global average? ~5%

Adding more context; India’s GNI (Gross National Income) grew at ~6% while China’s grew ~10%, most countries also found the growth to be closer to GNI +- 2%, so GNI growth > does lead to wealth growth.

Now wealth per adult is an “average”, i.e has an affect from outliers, if you’d like to adjust for wealth inequaity, median would be nicer; India’s median wealth back in 2000 was ~$1,150 and grew to ~$4100 in 2022; i.e the median wealth grew ~6% vs. the average wealth per adult which grew at ~7.5% in the same period.

Now if that sounded like a lot of numbers; here’s the simpler takeaway;

Wealth per adult often grows similar to growth in income; China’s wealth per adult hence grew quite fast in the past few years, while India wasn’t much behind and didn’t do too shabby vs. global average

Given the expectations in India’s income in the upcoming year, the above also bodes for good news

However wealth inequality does exist and this growth won’t be the same for all, while we may continue to do extremely well and overall people would become richer, the wealth would grow faster for the richer, and the average person’s wealth would grow at a slightly lower but still pretty fast pace.

By the way, did I mention, India on average has a slightly higher savings rate than the world? ~29% as of 2021, higher than the global average of ~27%

Now let’s move to 2) Where would this be invested?

Where would this be invested? (also Financialization of Savings)

Now let’s understand where people park majority of their money today - FDs, infact on an average Indians save INR 4.25L in FDs.

However, while historically, FDs may have been attractive, the trend is shifting, as households shift to assets that can offer higher returns over and above inflation, infact while FDs have managed to grow their AUM by a CAGR ~10% between 2017-22, the assets managed by the investment industry grew at 16% between the same period.

Thus, AUM of managed products as a % of deposits went from ~59% in 2017 to ~79% in 2022, however if you think this is high, the US in 2021 had this ratio at ~150% up from ~68% in 2001 and ~23% in 1991.

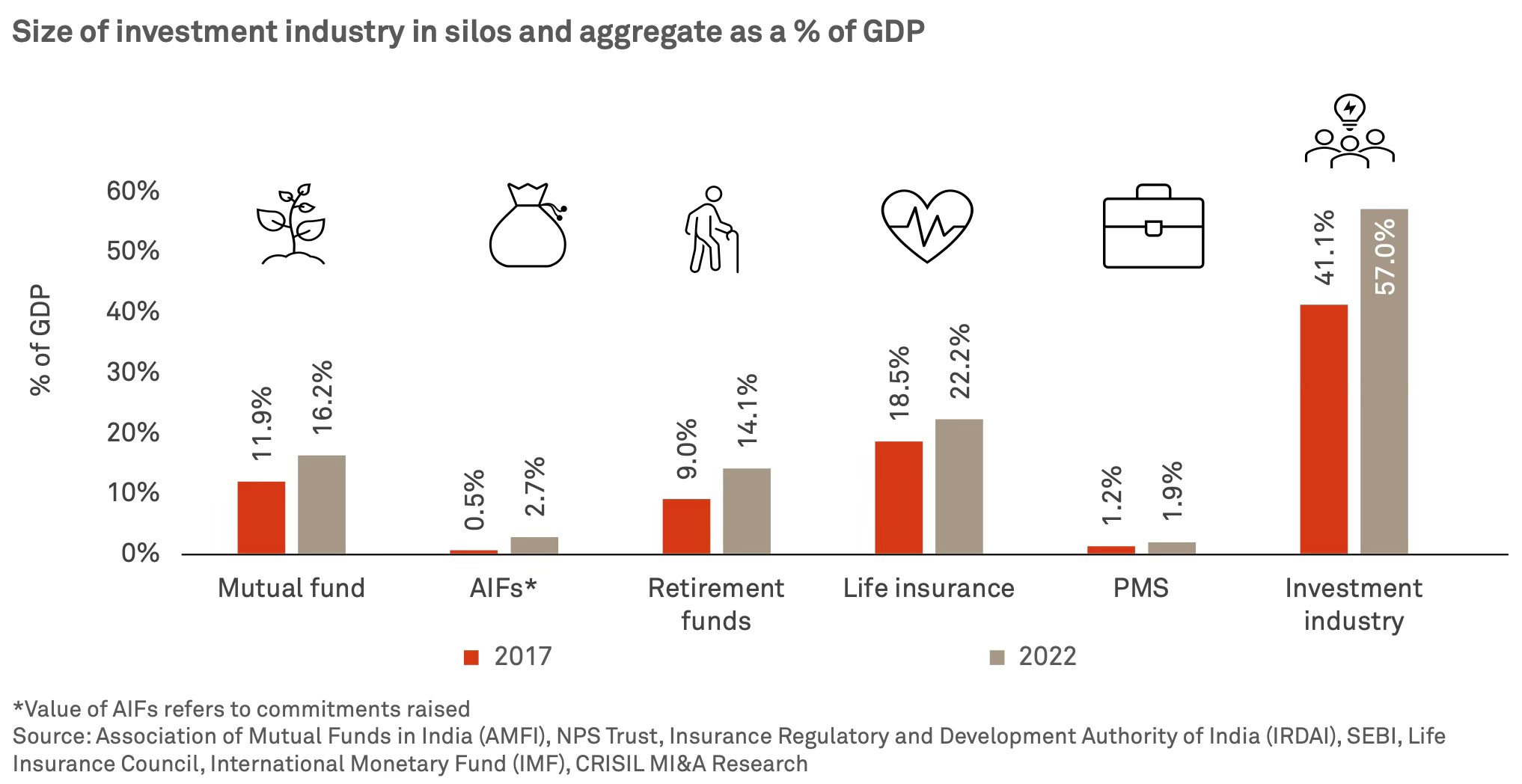

Now how much is exactly invested in financials assets by Indians? about INR 135 Lakh Crore or roughly ~57% of GDP as of 2022*, back in 2017, this was only ~41% of GDP and is expected to be ~74% of the GDP in 2027

do note GDP is an annual number while the assets being managed today are as of today, accumulated over time

Coming to where this managed money is at; the largest chunk is actually insurance schemes (yeah, really, them insurance agent uncles with their feet on street actually grt alot done); managing ~INR 52 Lakh Crore of those assets, or ~39% back in 2022.

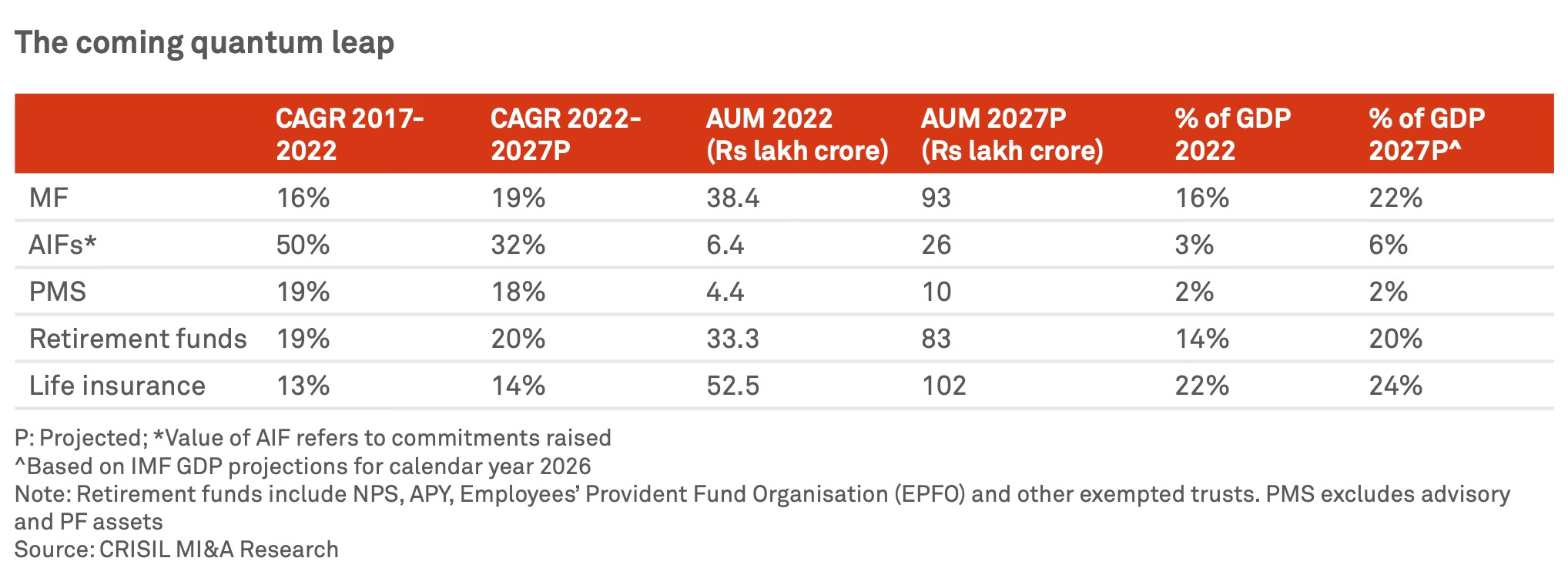

Mutual funds with ~INR 38 Lakh crore in 2022 were at 28.4%, in 2024, this number is at a whopping INR 54 Lakh Crore.

But here’s more; AIFs (Alternative investment funds) - which as the name suggests invest in alternaitve assets and include funds like VCs, PEs, Hedge Funds, etc., saw their AUM growth at 50% CAGR between 2017-22.

Here’s a nice chart in a report by crisil to highlight on these assets as % of GDP

Okay, so income is going to increase > people will spend and save > money will be investing in financial assets > but which ones?

Now as a % of GDP? probably the mass targeted ones like mutual funds and pension schemes like NPS.

But growth in AUM? AIFs

This comes as little surprise; given that while the middle class will expand, the ones who’d contribute alot more to investing in financial assets in absolute terms are the rich, who, as the wealth per adult and median wealth levels indicate, will see their wealth rise faster too at a bigger base.

Now, what are the final takeaways here?

Takeaways

The main takeaway (especially for me) is that India’s investment industry is going to really see a rush in its assets, and while it’s easy to think this phenomena of people investing is temporary basis the recent bull runs, the surge of finfluencers and more ads than ever, the data points to this as being more of a structural story for the next 5-10 years, in fact it is the negative sentiments and slow down during bearish periods which would be temporary in India’s journey of financailization of savings in the near future in my view.

What’s MORE amazing is that it’s not just going to be mutual funds but alternatives are going to get their fair share and the industry as a whole is going to become deeper in their offerings, which not only means more diverse options for investors (yay) but also more career opportunities.

What’s perhaps not that optimal from an emotional POV is that the surge in income and wealth won’t be equal and they’d still be wealth inequality, however the people as a whole would be richer in 5-10 years vs. today, which is still amazing news!

But here’s a lingering question; given we already struggle with market breath in public markets and the deal flow in private markets have been slow at best, especially in the later stages in the recent times, where will all this money be invested and at what terms?

Until next time, as always, keep manifesting wealth.

Makes obvious sense to plug in a friend’s super solid and growing firm here that’s all about managing your wealth

The Financialist is your go-to personal finance manager. Be it tax planning & filing, investment management, liabilities management & optimisation & insurance planning, The Financialist does it all in an integrated manner and the best part is since they charge you a fee, unlike others, they will tell you what's right for you (not mis-sell to make heavy commissions) and also, help you execute it.

Get on a free financial planning call with The Financialist here:

Disclaimer 1: All above views are purely for educational purposes and are not to be taken as investment advice. Investment or trades taken of any kind based on this are solely the person’s risk and I bear no liability. Please consult a financial advisor before making any investments. All investments are subject to market risks.

Disclaimer 2: The views presented above are mine and not of any organization(s) I work with / am employed at

Sources: