Trying to figure out which stage of market cycle we are in - Q1 FY25

Trying to figure out which stage of market cycle we are in - Q1 FY25

Studying Equities, Bonds and Commodities

Hi,

Recently, with US inflation remaining sticky, there’s news that rate cuts could be further delayed (Source)

Now back in the day, I had written why rate hikes may not be the best solution to US inflation back then

However, today’s article is an attempt to do what’ve done in the past too, engage in the exercise of where - Equities (Stocks), Debt (Bonds) and Commodities (Gold, Steel, etc.) will go from now.

The look-back here I’m taking is YTD(~3M) and 6M while also using ADX to gauge the strength of the trend here.

Let’s Begin

Performance of the Asset Classes Till Now

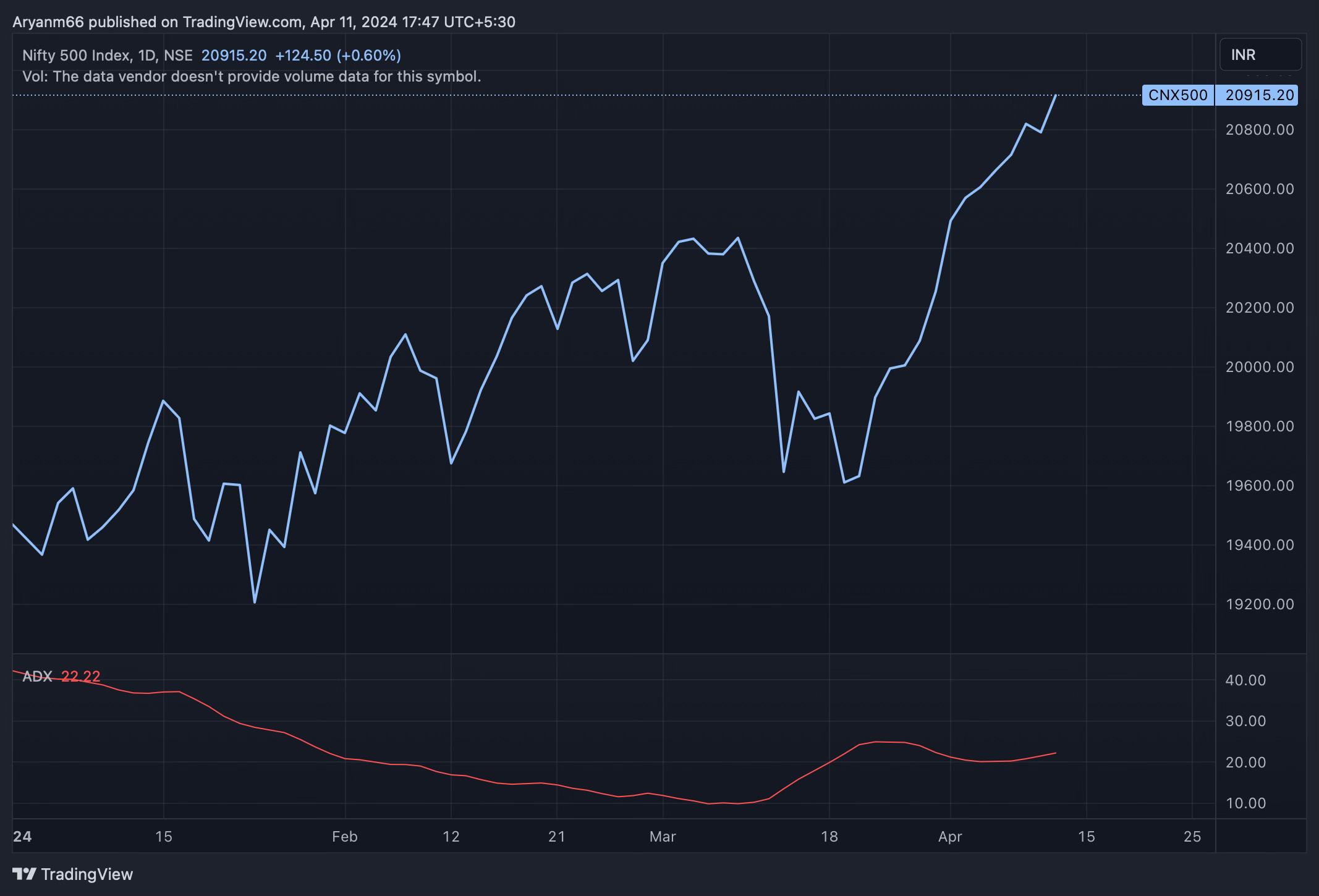

NIFTY 500

The NIFTY 500 (Proxy for equities); on a 6M timeframe has been on a strong upwards trend, also supported by the ADX > 40, however this momentum while still on, has seemingly slowed down (evident by ADX too, being between 20-25).

While there are concerns regarding the valuations of the index (more on that in a while), it’d be unfair to say there isn’t remaining momentum for a little bit while more.

India and US 10 Year Yields

If we were to zoom out, we see that usually IN10Y follows the movements of US10Y to a large extent, now this is not to say that that’s the sole factor, but over the 20Y, there’s an observation that US10Y movements do affect IN10Y to a certain extent.

Now if we see the US10Y for the past 6M, it has seen it’s yields which originally were declining, starting to rise up (From the start of the year), while there were expectations of rate cuts early this year initially, that no longer seems to be the case

Now if we see IN10Y, we’d see something similar beginning to emerge, the IN10Y yields has been majorly on the declining trend over the past 6M (Similar to the first half of the 6M trend in US10Y) and now has started to see that trend reverse.

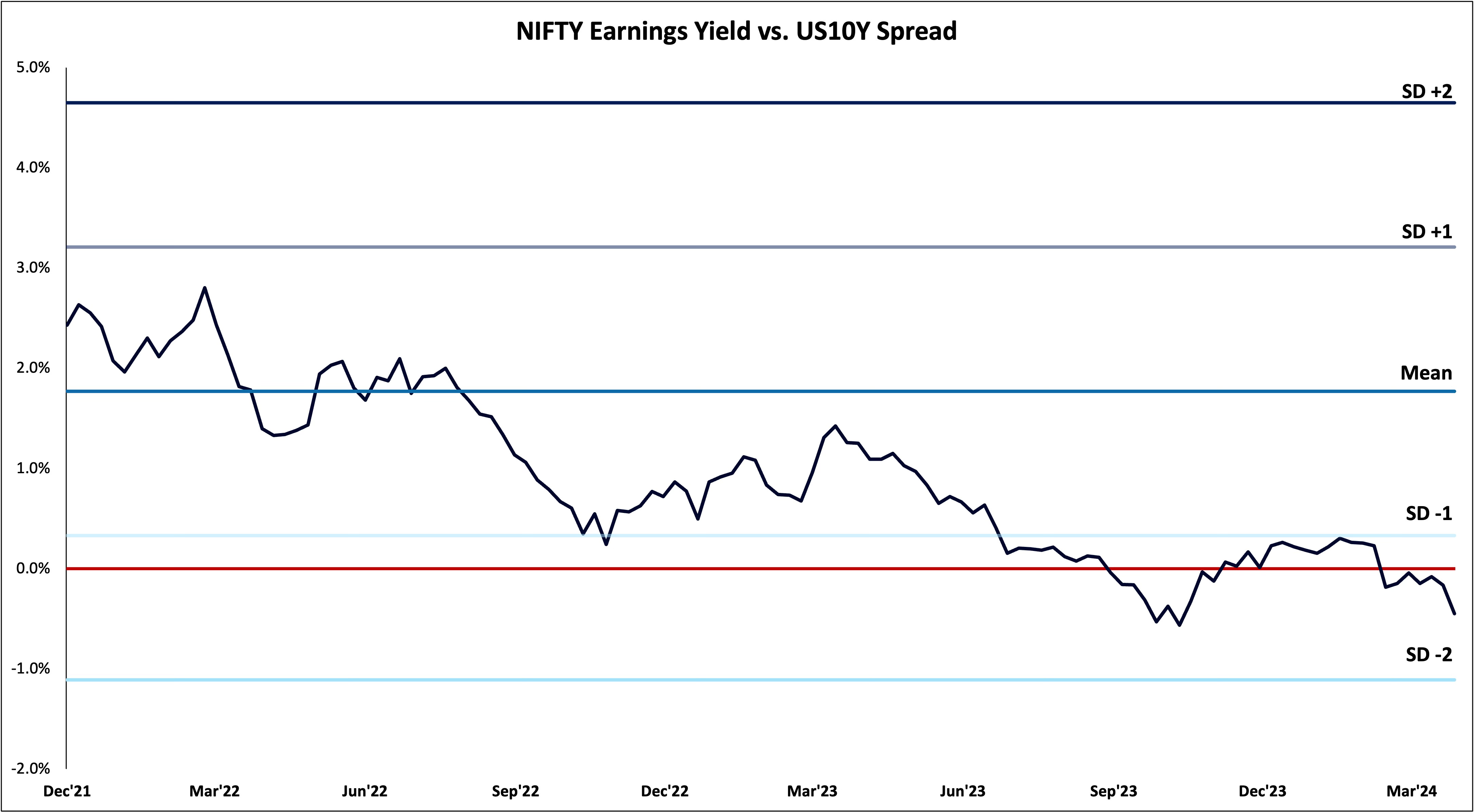

NIFTY 500 EY and IN10Y

Earlier, while talking equities, I mentioned a bit on the valuation concerns regarding the index, now if we look at the spread of NIFTY 500 Earnings Yield (reverse of it’s PE) with the US10Y, one would see a negative spread (i.e, the risk reward is actually quite off of investing in equities vs. bond), up till now, the assumption that rates would eventually get cut could’ve helped give a bit more positive perception about equities (if the yields went down, the spread would automically expand and it was true uptil a few weeks ago)

But now given we expect the yields to stay or even come back up a bit in the current trend (given the expectations has changed), it’s quite likely eventually stocks would be considered even more expensive down the line (this is important as we move down in the article and would make more sense then).

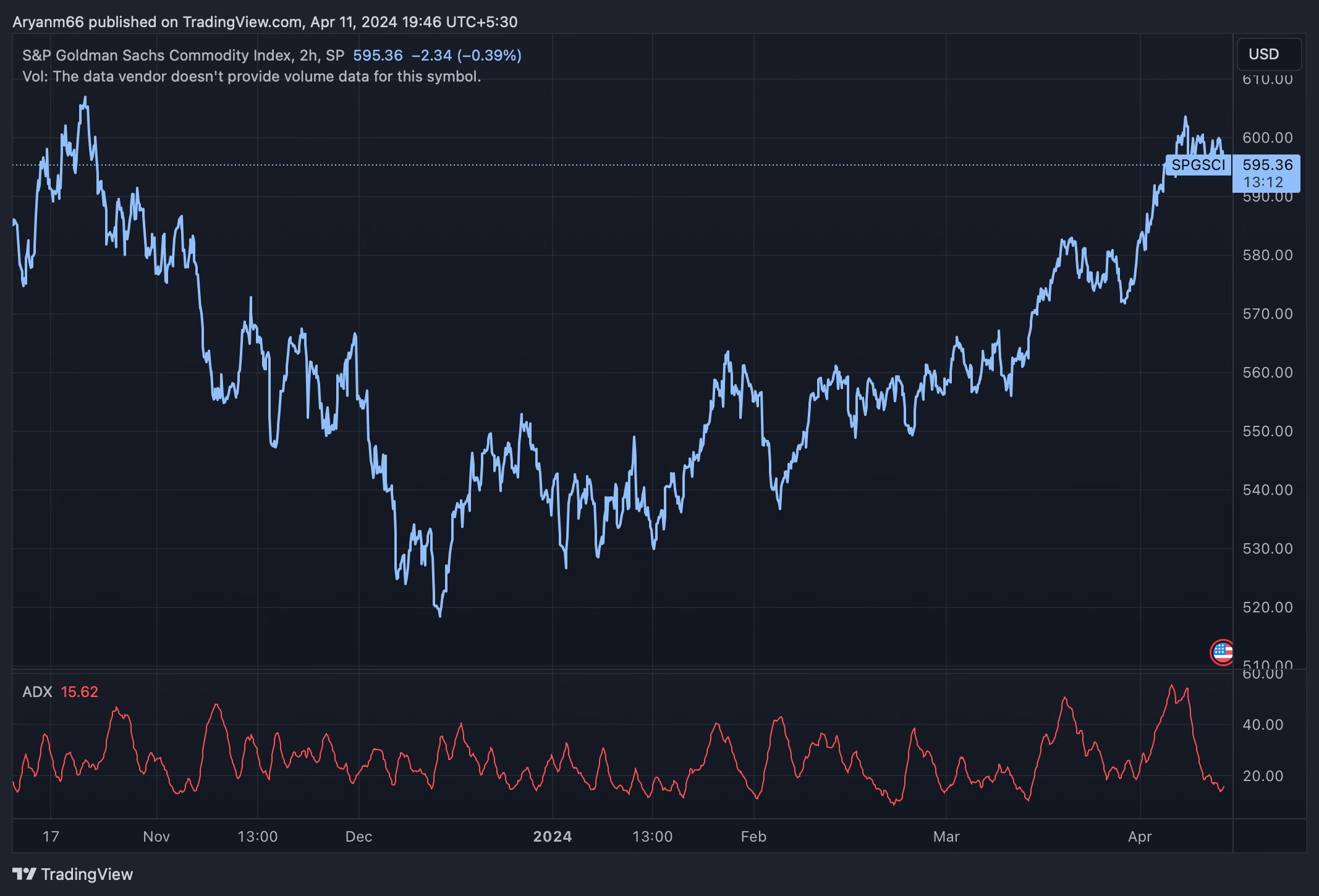

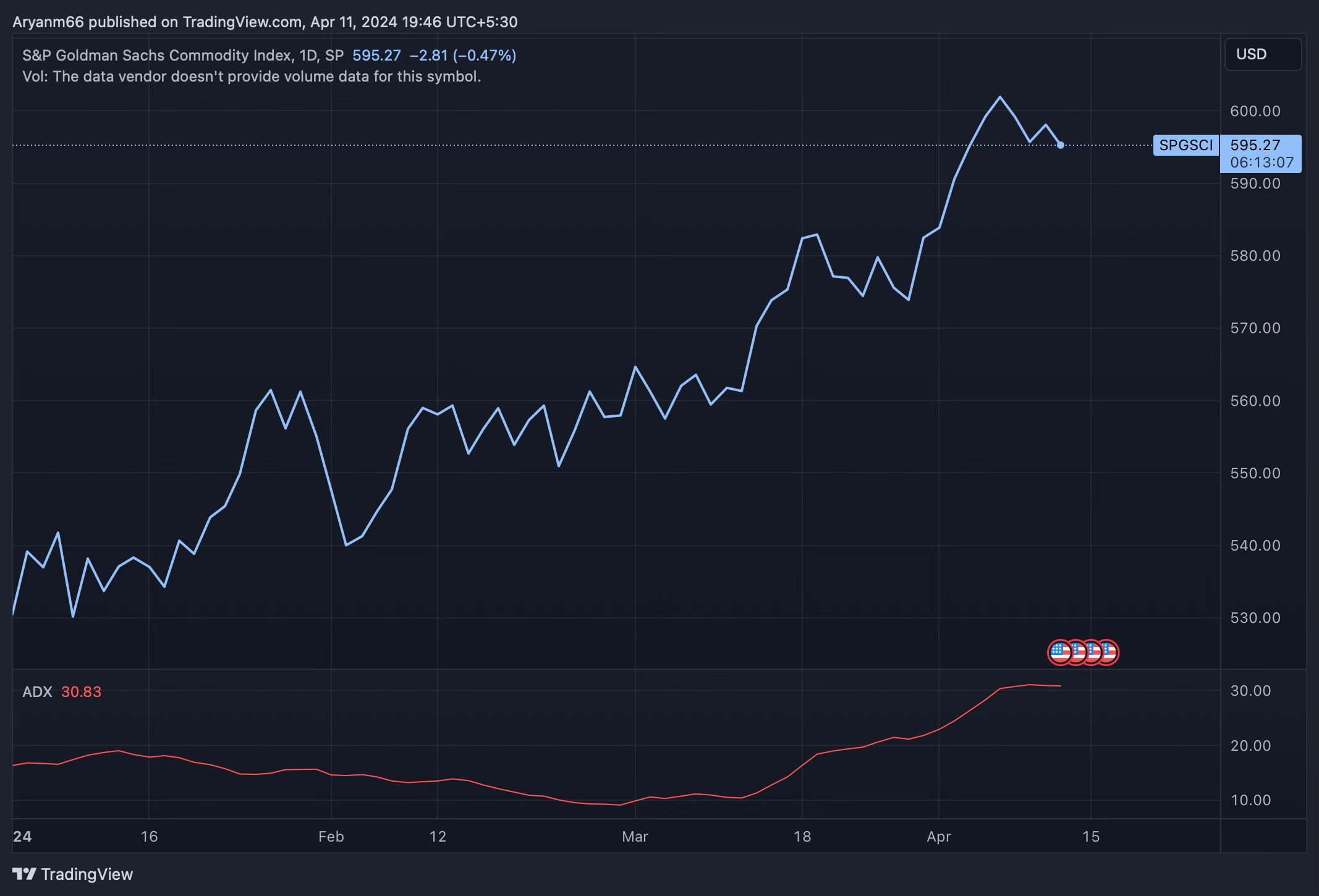

Commodities - S&P GSCI

An easy way to track commodities is through the S&P GSCI, it’s mostly driven by Energy (>50%) such as crude oil, refined oil, natural gas followed by grains (wheat, corn, soybeans) and Industrial Metals (Aluminum, copper, zinc, nikel, lead) which contribute >10%, and then contirbutions from Livestock, Precious metals.

This is ofcourse tracked in US$

Commodities based on the index have started to come back, with YTD being a strong trend that’s picking up pace as evident by the ADX too, which is now >25.

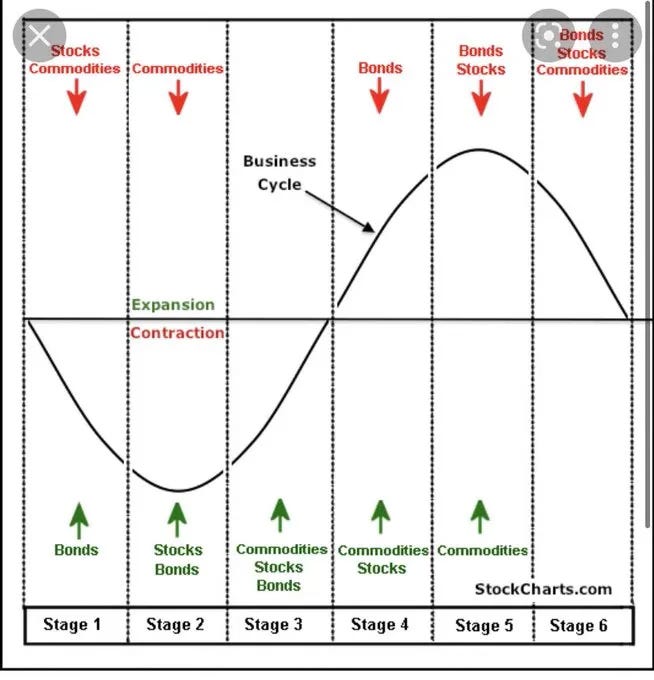

Putting it together and outlook

Let’s understand what we have here

Equities - Rising with a slowing momentum

Bonds - Have gone from rising to falling (given yields are rising) - emerging change in trend

Commodities - started to rise and picking up momentum

Based the points discussed and the chart above, one can conclude we are basically crossing over from Stage 3 to Stage 4 (from all asset classes rising, to bonds starting to decline while stocks and commodities continue to rise, before stocks follow suit), post which, we could see stocks declining.

Let’s see now how this plays out in a few months.

Until then, keep manifesting wealth.

Disclaimer 1: All above views are purely for educational purposes and are not to be taken as investment advice. Investment or trades taken of any kind based on this are solely the person’s risk and I bear no liability. Please consult a financial advisor before making any investments. All investments are subject to market risks.

Disclaimer 2: The views presented above are mine and not of any organization(s) I work with / am employed at

Sources:

Trading View